1. Regulaization Methods

- Regularization methods are based on a penalized likelihood :

- \(Q_{\lambda}(\beta_0, \beta) = -l(\beta_0, \beta) + p_{\lambda}(\beta)\)

- \((\hat{\beta_0}, \hat{\beta}) = arg min Q_{\lambda}(\beta_0, \beta)\)

- Penalized likelihood for quantitive

- Linear regression model : \(y_i = \beta_0 + x_i^T \beta + \epsilon_i\)

- l1-norm : \(\lambda \sum(\hat{\beta}^2)\)

- l2-norm : \(\lambda \sum|\hat{\beta}|\)

- \(Q_{\lambda}(\beta_0, \beta) = -l(\beta_0, \beta) + p_{\lambda}(\beta) = \frac{1}{2}\sum_{i=1}^{n}(y_i - \beta_0 + x_i^T \beta)^2 + p_{\lambda}(\beta)\)

- Penalized likelihood for binary

- CVE based on deviance : \(CVE = \frac{1}{n}\sum_{k=1}^K -2\sum_{i \in C_k}(y_i \log{\hat{p_i}^{[-k]} + (1 - y_i) \log{(1-\hat{p_i}^{[-k]})})} \)

- if type="response" : \(p_i(\beta_0, \beta) = \frac{e^{\beta_0 + x_i^T \beta}}{1 + e^{\beta_0 + x_i^T \beta}}\)

- CVE based on classification error : $CVE = \frac{1}{n}\sum\sum I(y_i - \hat{y_i})^{[-k]}$

2. [Ex] 2. Heart Data

# Importing Datasets

library(glmnet)

url.ht <- "https://www.statlearning.com/s/Heart.csv"

Heart <- read.csv(url.ht, h=T)

summary(Heart)

# Preprocessing Data

Heart <- Heart[, colnames(Heart)!="X"]

Heart[,"Sex"] <- factor(Heart[,"Sex"], 0:1, c("female", "male"))

Heart[,"Fbs"] <- factor(Heart[,"Fbs"], 0:1, c("false", "true"))

Heart[,"ExAng"] <- factor(Heart[,"ExAng"], 0:1, c("no", "yes"))

Heart[,"ChestPain"] <- as.factor(Heart[,"ChestPain"])

Heart[,"Thal"] <- as.factor(Heart[,"Thal"])

Heart[,"AHD"] <- as.factor(Heart[,"AHD"])

summary(Heart)

dim(Heart)

sum(is.na(Heart))

Heart <- na.omit(Heart)

dim(Heart)

summary(Heart)

# Train model

## Logistic Regression

# Add dummy variable to original matrix x wihtout intercept

x <- model.matrix(AHD ~., Heart)[,-1]

y <- Heart$AHD

# Train model

g1 <- glmnet(x, y, family="binomial")

# Comparison lambda - coefficient, l1-norm - coefficient

par(mfrow=c(1,2))

plot(g1, "lambda", label=TRUE)

plot(g1, "norm", label=TRUE)

df <- cbind(g1$lambda, g1$df)

colnames(df) <- c("lambda", "nonzero")

rownames(df) <- colnames(g1$beta)

df

- If lambda decreases, the number of active coefficients increase.

- If l1-norm increase(lambda decrease), the number of active coefficeints increase.

# Make evaluation : 10 folds

set.seed(1234)

K <- 10

n <- length(y)

fold <- sample(rep(1:K, length.out=n))

lam <- g1$lambda

MSE <- matrix(0, n, length(lam))

for (i in 1:K) {

test <- fold==i

tran <- fold!=i

g <- glmnet(x[tran, ], y[tran], family="binomial", lambda=lam)

prob <- predict(g, x[test, ], s=lam, type="response")

yval <- y[test]=="Yes"

MSE[test, ] <- -2*(yval*log(prob) + (1-yval)*log(1-prob))

}

CVE <- apply(MSE, 2, mean)

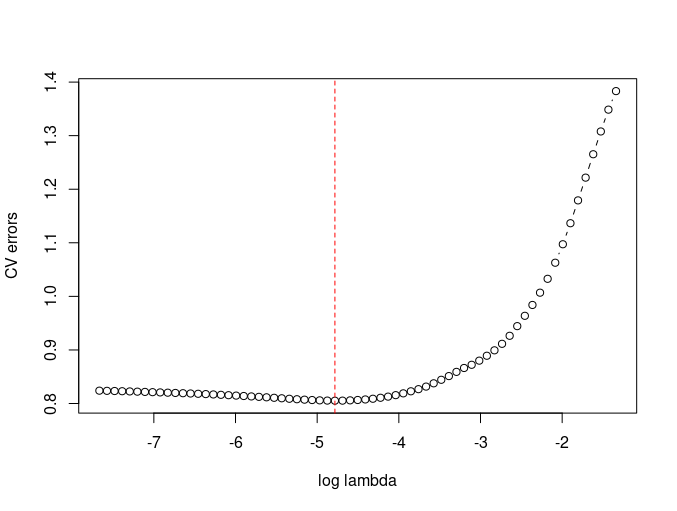

# Visualize CVE metrics

par(mfrow=c(1,1))

plot(log(lam), CVE, type="b", xlab="log lambda", ylab="CV errors")

abline(v=log(lam)[which.min(CVE)], col="red", lty=2)

# Make final model : With full training set

lam[which.min(CVE)]

coef(g, s=lam[which.min(CVE)])

g1 <- glmnet(x, y, family="binomial", lambda=lam[which.min(CVE)])

coef(g1)

- K-fold without using cv.glmnet.

- MSE has been used for model evaluation metrics.

- model.matrix function convert original data into categorical encoded columns and intercepts.

- To apply this metrx to glmnet, we need to input matrix without intercept.(beacuse inner argument of intercept is True).

- However, if we calculate prediction from the result of coef function, then we need to multiply with matrix with intercept.

3. [Ex] Heart Data with automatic CV

set.seed(123)

par(mfrow=c(1,3))

# Error metric : Deviance

# foldID shows the restricted fold -> don't need to use nfolds parameters

gcv1 <- cv.glmnet(x, y, family="binomial", lambda=lam,

nfolds=5, type.measure="deviance")

plot(gcv1)

# Error metric : Classification error

gcv2 <- cv.glmnet(x, y, family="binomial", lambda=lam,

nfolds=5, type.measure="class")

plot(gcv2)

# Error metric : ROC-AUC score

gcv3 <- cv.glmnet(x, y, family="binomial", lambda=lam,

nfolds=5, type.measure="auc")

plot(gcv3)

c(gcv1$lambda.min, gcv1$lambda.1se)

c(gcv2$lambda.min, gcv2$lambda.1se)

c(gcv3$lambda.min, gcv3$lambda.1se)

g0 <- glmnet(x, y, family="binomial", lambda=lam)

coef(g0, s=c(gcv1$lambda.min, gcv2$lambda.min, gcv3$lambda.min))

coef(g0, s=c(gcv1$lambda.1se, gcv2$lambda.1se, gcv3$lambda.1se))

- Three plots are written based on one-standard error.

- The left vertical line is the value of gcvl$lambda.min.

- The right vertical line is the value of gcvl$labmda.1se.